Alphabet's Full-Stack Compounding

Mornings With Markman - May 12th, 2026

The Economics of Alphabet’s Full Stack

It was only three years ago when investors wrote off Alphabet in the future of artificial intelligence. Back then, ChatGPT seemed to be building an insurmountable lead. Despite developing the underlying transformer technology, Alphabet was widely viewed as old and slow-footed. What investors missed is the power of vertical integration. Now, the dynamism of that full stack is creating a virtuous cycle.

Control over every layer of production, from custom silicon to consumer applications like the Gemini AI model, provides a unique structural advantage. This strategy removes reliance on third-party hardware vendors for internal workloads and allows total ecosystem control. Bringing these operations in-house transforms Alphabet from a single-service provider into a self-contained industrial entity. A well-run business can simultaneously optimize hardware and software.

Refining custom Tensor Processing Units for over a decade has created a formidable bedrock for cost-efficiency. According to the fourth-quarter 2025 financial results, internal optimizations reduced the serving costs of Gemini by 78%. This massive efficiency gain allowed Alphabet to absorb rising usage without a commensurate increase in capital spending. The AI business is now subsidizing innovation through proprietary hardware.

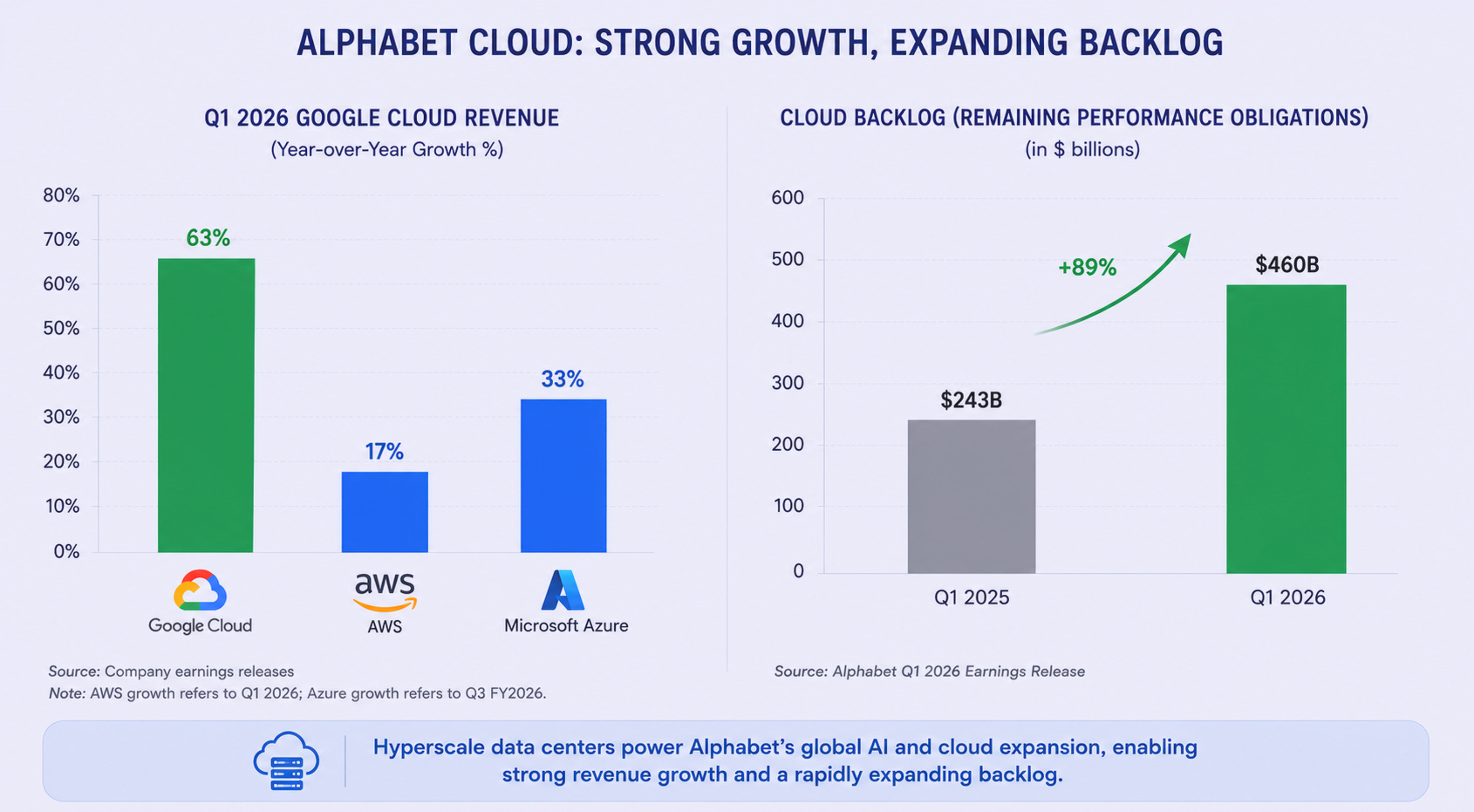

Hyperscale data centers provide the physical engine for this global deployment. In Q1 2026, Google Cloud revenue surged 63% year-over-year to $20 billion, outdistancing major competitors by a wide margin. The cloud backlog nearly doubled to $460 billion, proving that enterprises are gravitating toward this integrated platform. Meanwhile, Alphabet is scaling Gemini across Search and YouTube without paying a middleman tax for external compute power.

The result is a virtuous cycle hitting on all cylinders.

Increased usage across search generates data that informs the design of next-generation custom silicon like the Axion CPU. This new chip offers 30% better price-performance than other hyperscale providers for agent runtimes. Each successful iteration lowers the cost of the next innovation. This self-reinforcing loop widens the gap between Alphabet and the rest of the market.

Early fears regarding capital expenditure growth have also proven unfounded. While investors worried these costs would compress margins and punish shareholders, consolidated operating margins actually expanded to 36.1% in Q1 2026. This performance proves that vertical integration generates superior operating leverage. Alphabet is no longer merely a software provider; it has become an integrated industrial powerhouse with unmatched fiscal resilience.

The company is building a defensive moat that is increasingly difficult for newcomers to storm. Competitors focusing on single layers of the technology stack remain vulnerable to supply chain bottlenecks and third-party pricing whims. Because Alphabet controls the entire experience, it can maintain a level of quality and cost-efficiency that fragmented competitors cannot match. This structural lead is how the company caught and surpassed ChatGPT.

Alphabet shares are up 350% since January 2023. We are proud that we saw then what other investors missed in the euphoria of ChatGPT. Years later, the value of the integrated ecosystem is obvious. The narrative reversal is complete as the company moves from a perceived defensive incumbent to an assertive industrial powerhouse. Alphabet is now the primary beneficiary of the new computational economy. Longer-term investors should use weakness to accumulate shares.